For the last few months, businesses around the world have had to rapidly adapt to the impact of COVID-19.

In a time where it seems like things change every day, it can be difficult to gauge whether the challenges your business is facing are widespread.

That's why we're publishing week-over-week benchmark data for core business metrics like website traffic, email send and open rates, sales engagements, close rates and more. These core metrics are split by region, company size, and industry cuts so you can explore on your own to see data for companies most similar to your own. You can find the data, and more context on the dataset and sources, here.

Because the data is aggregated from our customer base, please keep in mind that individual businesses, including HubSpot's, may differ based on their own markets, customer base, industry, geography, stage, and/or other factors.

These insights are refreshed every Thursday morning ET, and will be accompanied by this short writeup. You can find past writeups using this timeline.

We hope to establish useful benchmarks to measure your business against, and serve as an early indicator of when short- or long-term adjustments may be needed in your strategy.

We hope to establish useful benchmarks to measure your business against, and serve as an early indicator of when short- or long-term adjustments may be needed in your strategy.

What We're Seeing

Here are the three key takeaways from the most recent week's data:

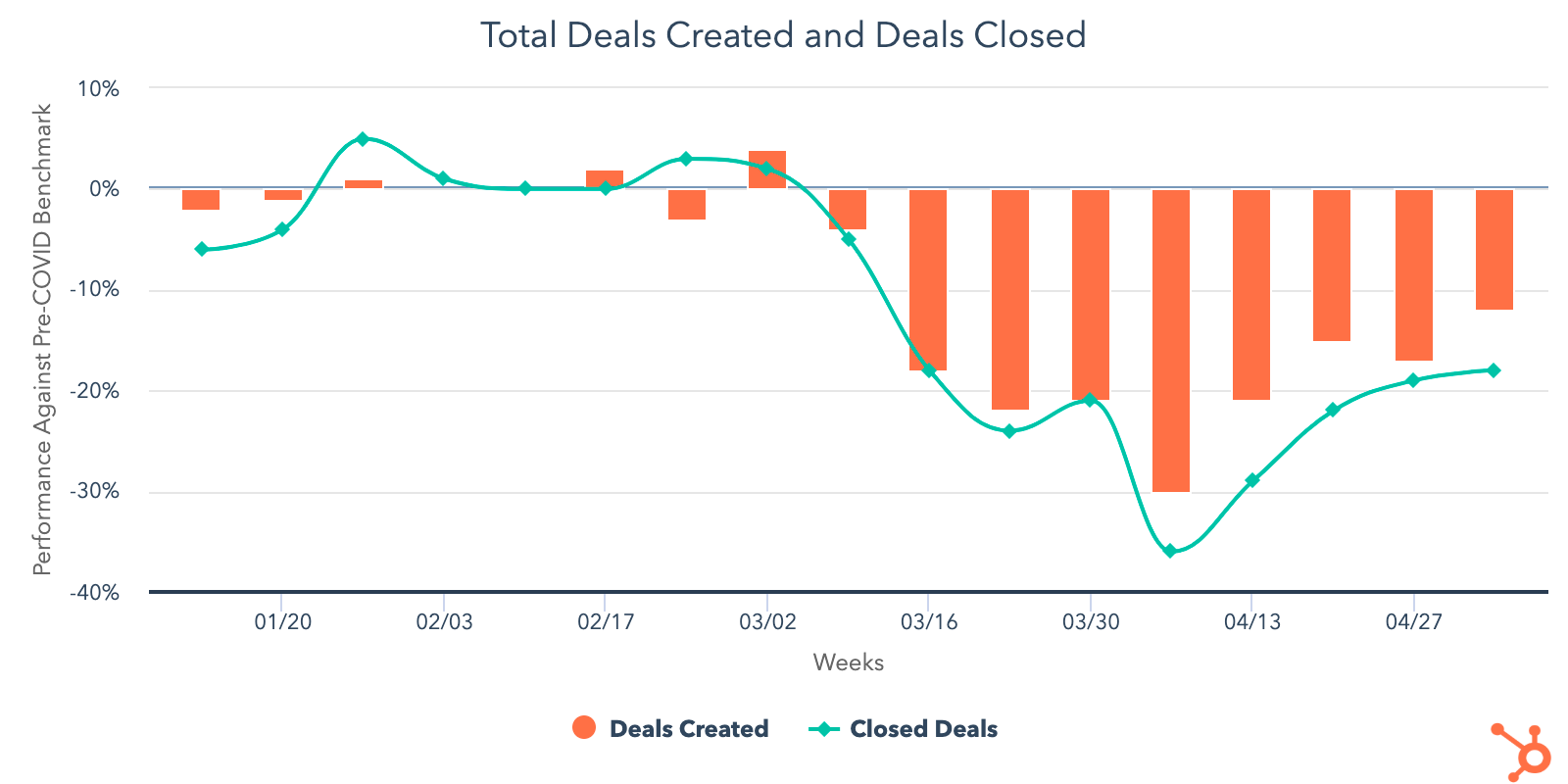

1. New deal creation is trending positively week-over-week, with some countries and industries trending above global averages.

The volume of new deals created globally increased 6% week-over-week. While this is 12% below pre-COVID levels, when compared to the previous low of 30% below pre-COVID benchmarks during the week of April 6, this metric is trending in the right direction. We hope the last few weeks of acceleration in deal creation will be reflected in closed-won deals in the second half of May.

After last week's drops in deals created, all industries we're tracking experienced an increase the week of May 4. Interestingly, four out of the seven had deal creation volume close to or above pre-COVID levels. Computer software is slightly below pre-COVID averages, while manufacturing (+2%), consumer goods (+8%), and construction (+8%) have slightly exceeded pre-COVID levels. The other three industries -- travel, human resources, and entertainment -- have been structurally impacted by COVID-19 and are keeping global averages low. All industries are still trending below pre-COVID averages for closed-won deals.

There's also some promising signs in countries that have begun reopening parts of their economy. Germany, Italy, and Spain are all seeing an acceleration in sales activity above global averages. In Germany, the volume of new deals created increased 14% and closed-won deals increased 16% last week. Italy saw a 23% increase in new deals created, and a 5% increase in closed-won deals. Spain had the largest week-over-week increases, with a 35% jump in new deals and 61% increase in closed-won deals. New Zealand and Australia largely held with global averages.

It's important to note that with the exception of Australia, where deal creation has nearly recovered to pre-COVID averages, these countries are all still trending below pre-COVID levels. The accelerations seen in Germany, Spain, and Italy are anchored by significant drops in these metrics in March. Explore macro regional data here.

Deal pipeline metrics are also available by company size.

2. Prospecting continues to increase across the board, while sales engagement is holding flat.

After a dip the week of April 27, email prospecting increased 7% the week of May 4. Call prospecting saw a 10% increase. Sales response rate was flat week-over-week, and is holding at 29% below pre-COVID levels.

Last week, the data suggested that sales teams were replacing the time they spent calling prospects with emailing instead, which has been ineffective in converting interest to date. Call prospecting typically acts as a forcing function for doing better research and pre-qualification, so we hope to see this balance shift back toward calling.

The volume of meetings booked saw a 5% lift week-over-week. This is somewhat encouraging, but would be more so if this increase was proportional to the higher volume of sales emails. For now, sales teams are still emailing at levels far above pre-COVID levels, and the corresponding increases in deals created and meetings booked shows that only a small portion of these efforts are paying off. This will not be sustainable in the long term, and we'll be watching closely over the next several weeks to see how downstream metrics like deals created and closed-won deals continue to shift as prospecting strategies evolve.

3. Newly available data on advertising spend reveals an opportunity for businesses that may have paused campaigns.

Globally, total advertising spend was 18% below pre-COVID levels the week of May 4, and has essentially been flat at that level since March 16. This trend held across all company sizes and most industries.

It’s understandable that advertising campaigns have been on pause for the last few months as businesses assessed their outlook. However, in that same time period, the volume of marketing emails has reached 33% above pre-COVID benchmarks, while engagement with those emails has exploded to 20% above pre-COVID averages. Marketers are putting a very small amount of money back into advertising campaigns, but we’re a little surprised that more investment hasn’t been made here at a time when marketing engagement has been steadily increasing, and when businesses seem to be regaining some sales velocity.

Perhaps unsurprisingly, consumer goods is the only industry trending above pre-COVID levels for ad spend. This makes sense given the transition from offline to online that many businesses have made out of necessity in the last few months.

What This Means for Businesses

Sales teams need to reinvent how they prospect.

While sales results are incrementally improving week-over-week, salespeople are still spending a great deal of time reaching out to poor-fit prospects. The deal pipeline metrics are an encouraging sign that more businesses are reentering buying processes, but it's still too early to tell how much of this growth will be sustained. For now, it's a safe bet that your sales team should continue prioritizing high-interest, good-fit buyers rather than indiscriminately prospecting.

Resources to Help

- Watch the replay of our Adapt 2020 webinar on selling through uncertainty

- Refresh your email outreach with these sales templates.

- Start using video in your sales outreach to engage more prospects.

- Use this guide to increase your sales close rates.

- Lead with empathy in sales emails to build rapport and increase response rates.

Consider whether online advertising is a fit for your business.

The significant dip in advertising spend tells us that many businesses have paused their ad campaigns either temporarily or indefinitely. There's an opportunity for companies to enter a more affordable market. Whether or not this approach is right for your company entirely depends on your audience and offering, but if online ads work for your business, now may be a good time to un-pause campaigns.

Resources to Help

- Attend next week's Adapt 2020 webinar on advertising with empathy during a crisis.

- Get up to speed on using Facebook Lead Ads with this beginner's guide to building audiences and ads.

- Read our ultimate guide to online advertising.

- Plan your investment with this guide to budgeting for advertising.

- Set up and run campaigns using HubSpot Ads, Facebook Lead Ads, or Google Ads.

Free Software to Get Started

- HubSpot CRM is free and comes with included advertising and sales acceleration tools, including free 1:1 video, meetings, and chatbot tools.

- Gmail and Google Calendar integrations with HubSpot

- Zoom integration with HubSpot

- LinkedIn Sales Navigator integration with HubSpot

- Check out what HubSpot's app partners are offering at this time with this list of relief initiatives.

from Marketing https://ift.tt/3dHuUaI

via

No comments:

Post a Comment